RedBook’s Marque Equity Index highlights the automotive brands leading (and lagging) in market sentiment and value retention, showcasing those capturing industry confidence and those facing new challenges in 2025 and beyond.

What is the Marque Equity Index (MEI)?

The RedBook MEI is a proprietary metric that quantifies the relative strength of automotive brands in the Australian market. It distils complex market dynamics into a single, understandable score, enabling industry professionals to confidently compare brands. MEI is updated regularly to reflect current market conditions, providing actionable insights for pricing, inventory management, and strategic planning.

How is MEI Calculated?

- Data Sources: MEI draws on RedBook’s extensive database of retail, private, wholesale, and trade-in transaction data, including auction results, dealer sales, and fleet disposals.

- Sales-Weighted Approach: Each brand’s score compares the average retained value of its vehicles against the segment average, adjusted for sales volume and model mix.

- Index Interpretation: MEI scores show how a brand’s value retention compares to direct competitors within the same segment, highlighting relative strengths and weaknesses.

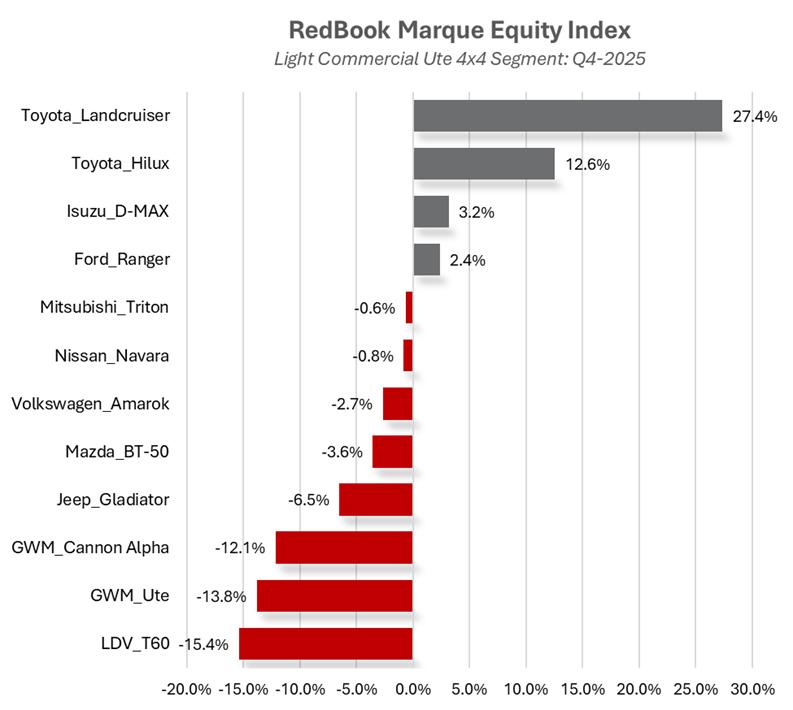

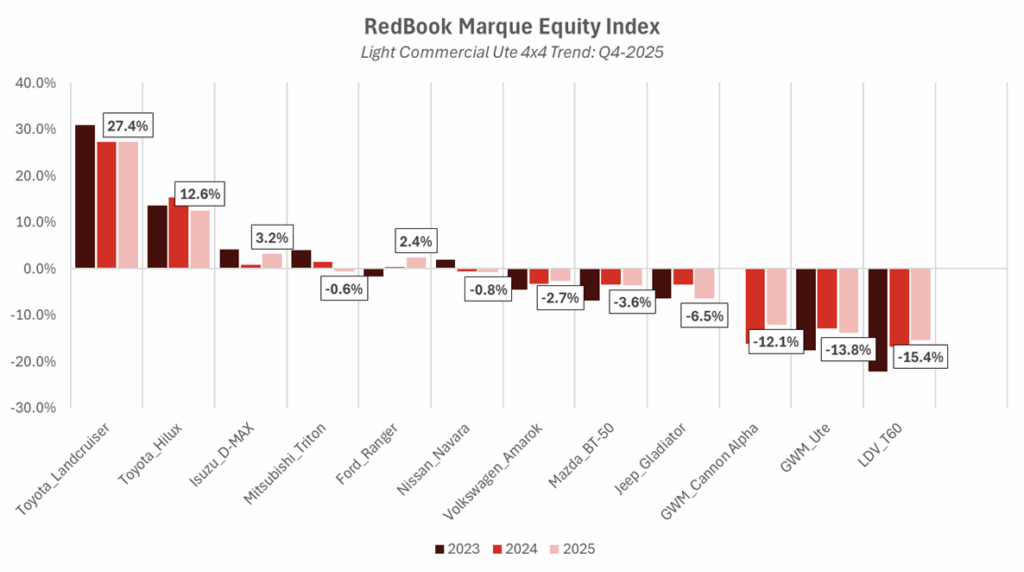

Market Overview

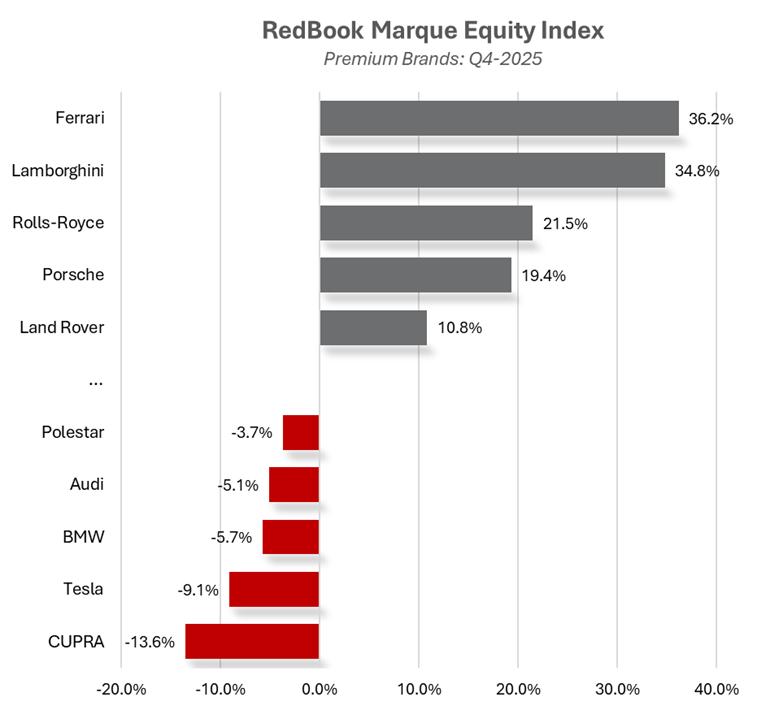

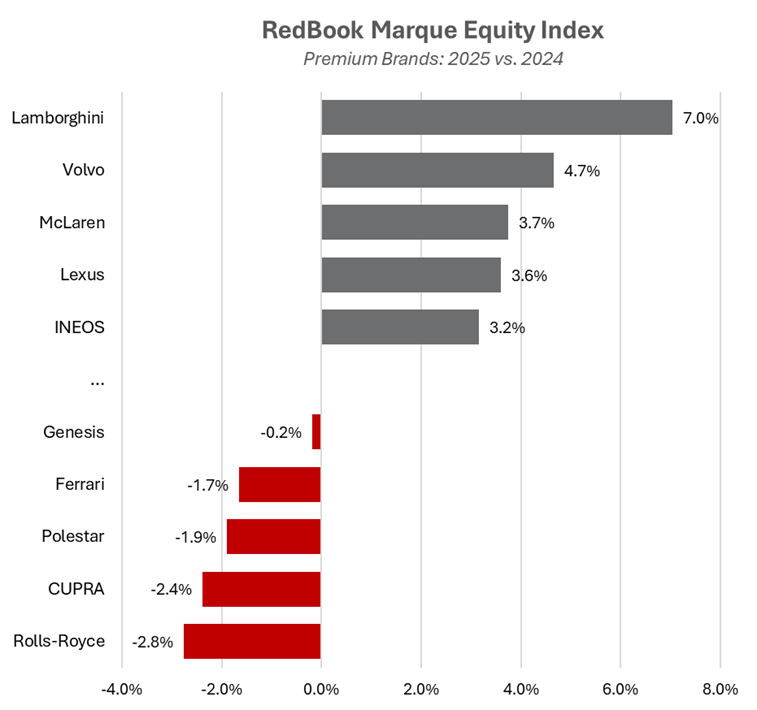

The 2025 RedBook MEI reveals an evolving environment for automotive brand equity in both mainstream and premium segments. Brand equity remains a key factor influencing residual values, fleet decisions, and dealer operations. This year’s results show significant movements across brands, emphasizing the importance of strategic brand management and adaptability.

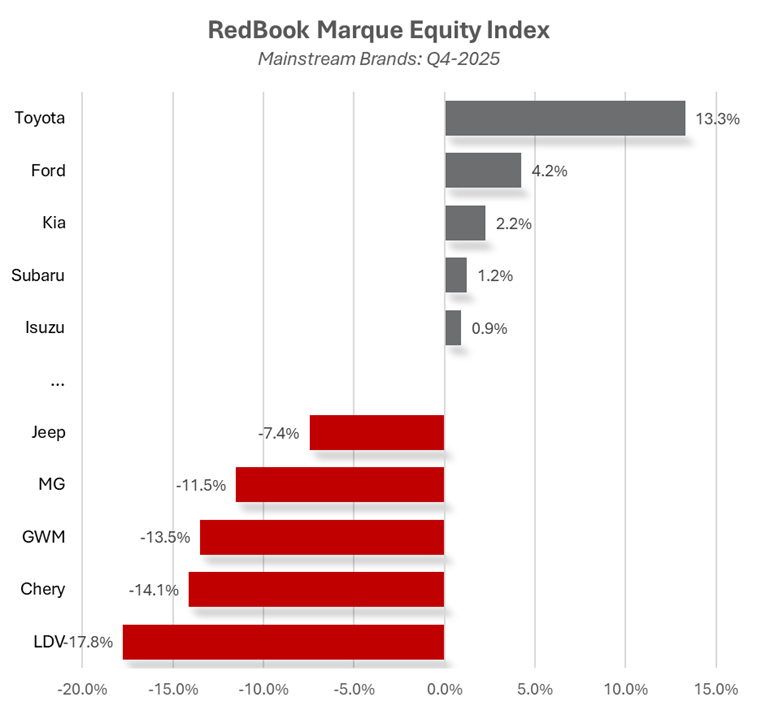

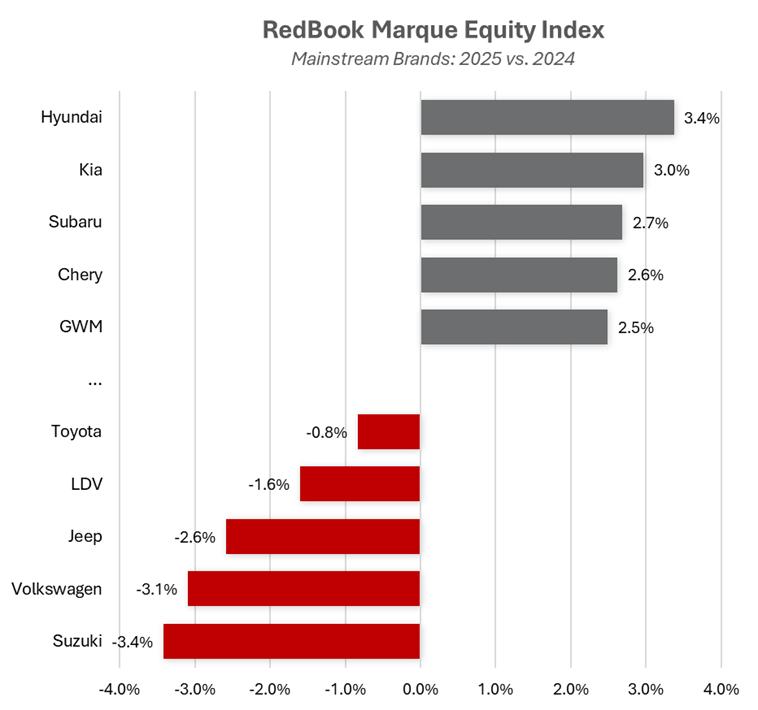

Mainstream Segment: Winners and Challengers

The mainstream market is shaped by both emerging and established players. LDV, Chery, GWM, MG, and Jeep occupy the bottom five positions, with LDV at -17.8%, reflecting ongoing challenges in price retention. These brands face headwinds from market perception, supply chain volatility, and competition.

Toyota leads with a 13.3% index value, reinforcing its reputation for strong residuals and dealer confidence. Ford, Kia, Subaru, and Isuzu also show positive momentum, indicating effective product strategies and sustained demand.