The New Vehicle Efficiency Standard (NVES) transitioned from policy to commercial reality on 1 July 2025, marking the start of the first compliance performance period. . Almost nine months in, the impact is tangible: NVES is successfully steering OEM powertrain strategies, yet it faces a market where utes and heavy-duty, fit for purpose vehicles remain firmly at the centre of Australian buyer demand.

The NVES framework effectively turns fleet-average CO2 performance into a tradable cost: brands that exceed their target can accrue a liability (and ultimately face a penalty), while brands that beat target can generate credits. The NVES Regulator’s first published performance-period results for 2025 (covering 1 July to 31 December 2025) has increased transparency on which OEM model mixes are tracking above or below target and that transparency is flowing quickly into product and pricing decisions.

Measured locally by way of interim emissions values (IEVs) NVES penalises car-makers that exceed fleet-average CO2 limits while rewarding those that come in under the mandated thresholds. In practice, NVES can create a real competitive advantage for brands with an EV/low-emissions-heavy line-up (or strong hybrid/PHEV mix) as evidenced by Tesla in the US, because they’re more likely to beat their fleet targets and generate credits while brands weighted to high-emitting SUVs, Utes and performance models can accumulate liabilities. That’s not necessarily “artificial” so much as “designed”: the mechanism intentionally rewards lower-emissions supply and makes a higher-emissions mix more expensive.

For more detail on which brands hold the cards by way of IEV credits, our compatriots over at carsales have compiled a nice summary of who’s in the red and those with the upper hand.

Even as OEMs recalibrate for NVES, Australia’s preference for SUVs and Utes continues to dominate the national sales chart. VFACTS reporting for 2025 shows another record year of new-vehicle sales, with the Ford Ranger finishing as Australia’s top-selling vehicle (56,555 units) for the third year running; a signal that the workhorse Ute remains a cornerstone purchase, not a niche indulgence. Early 2026 results reinforce the theme: February 2026 VFACTS reported 90,712 registrations for the month, with Ranger (4,325) and HiLux (3,625) again leading the model rankings.

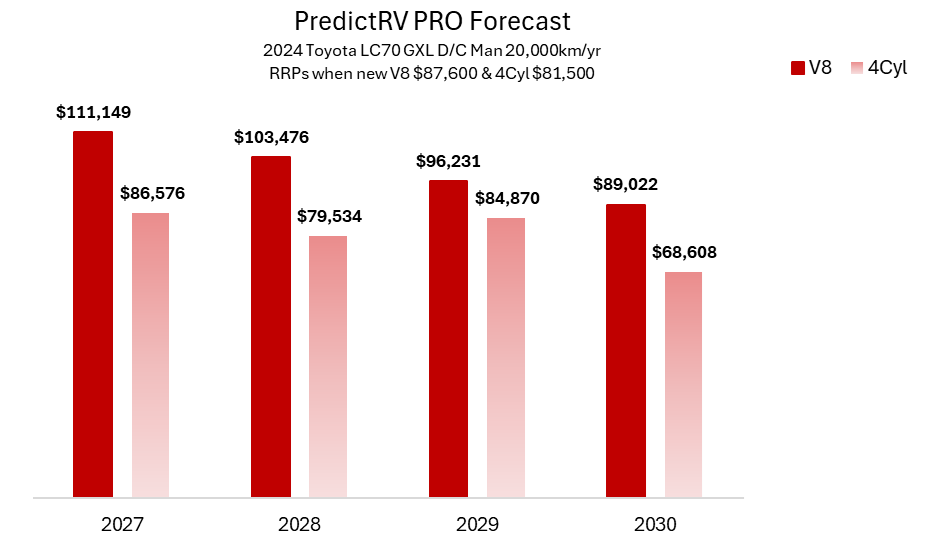

In our July RedBook Insider newsletter, we flagged the risk that policy pressure and limited replacement options could elevate residual values for specific, mission-critical vehicles. Six months into the NVES penalty window, that theme is being echoed in the broader market narrative: multiple industry outlets have reported sharp rises in used LandCruiser 70 Series pricing, particularly around V8-powered variants (no longer available), but even for the far less muscular but potent 4 cylinder on the back of ongoing demand for proven heavy-duty capability. Tools like RedBook’s industry leading PredictRV PRO illustrate how profound this “future classic” type residual position could be and it isn’t just isolated to Toyota.

The gap isn’t a lack of intent; it’s physics, infrastructure and product cadence. A genuine LandCruiser/Ranger Super Duty/Ineos-style replacement needs to deliver payload, towing, long-distance range under load, genuine off-road capability and rapid refuelling/charging in remote conditions. Battery-electric solutions in this space face trade-offs around weight, cost and range when working hard, while PHEV options are emerging but still limited in model availability and configuration. Some local retrofit programs (often targeted at mine sites) hint at what’s possible, but broad-scale, showroom-ready solutions at volume are still in transition.

NVES is already doing what standards are designed to do; pushing OEMs to re-think their model mix and accelerate lower-emissions powertrains. But Australia’s vehicle demand is still anchored in utility-led segments where fit-for-purpose alternatives remain scarce, and early-2026 VFACTS model rankings continue to be led by Utes. The next 12-24 months will be telling: do we see meaningful increases in PHEV/HEV availability in Utes and heavy-duty SUVs, or does the compliance pressure simply re-price the vehicles Australians keep buying?

Share this article:

Disclaimer:

The information presented in this article is true and correct at the time of publishing. business.carsales.com.au does not warrant or represent that the information is free from errors or omissions. The content is provided for informational purposes only and should not be construed as professional advice. For more details on our editorial standards and ethical guidelines, please visit our Editorial Guide Lines.